|

시장보고서

상품코드

2072761

통합 마케팅 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Integrated Marketing Services Market - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

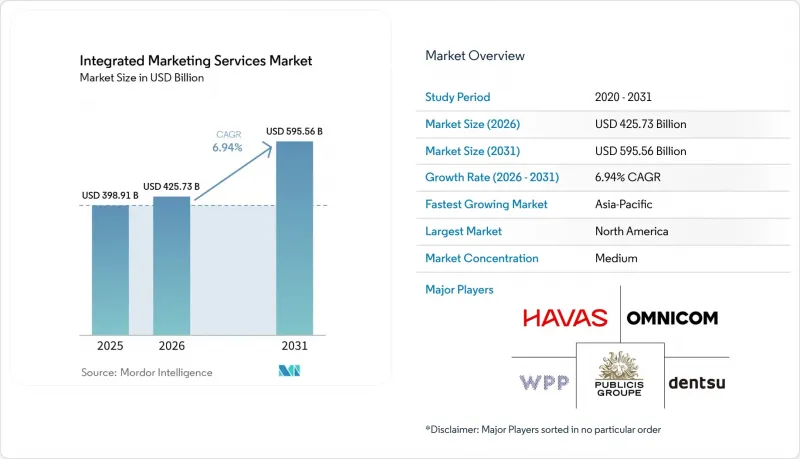

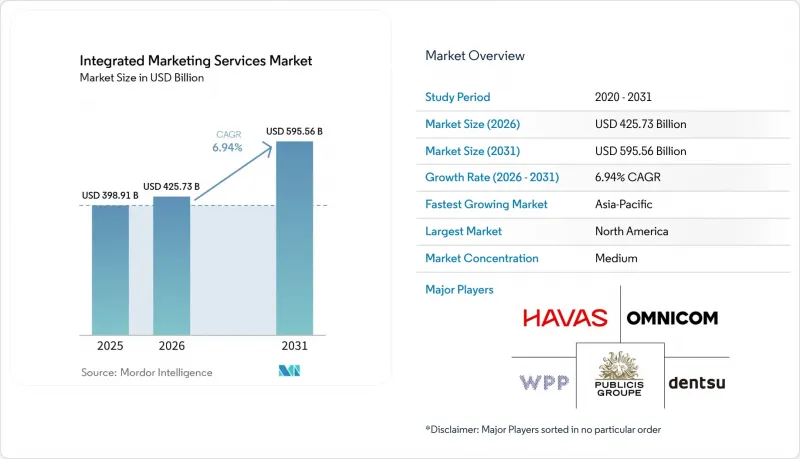

Mordor Intelligence에 의하면, 통합 마케팅 서비스 시장 규모는 2025년 3,989억 1,000만 달러로 평가되었고, 2026년에는 4,257억 3,000만 달러로 추정되고, 2031년까지 5,955억 6,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 6.94%로 성장할 전망입니다.

본 보고서는 서비스 유형별(브랜드 전략 및 크리에이티브 서비스, 디지털 마케팅 서비스 등), 제공 모델별(프로젝트 기반 계약, 리테이너 기반 계약 등), 조직 규모별(중소기업 등), 최종 사용자 산업별(소매 및 전자상거래 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 통합 마케팅 서비스 시장 동향 및 인사이트

AI를 활용한 개인 맞춤화가 광고 대행사의 가치 제안을 재구축하고 있습니다.

인공지능(AI) 덕분에 타겟 고객 분석부터 캠페인 실행까지 걸리는 시간이 단축되고 있으며, 이러한 변화가 통합 마케팅 서비스 시장의 비즈니스 모델을 변화시키고 있습니다. 2026년, CMO(최고 마케팅 책임자)는 마케팅 총예산의 15.3%를 AI 이니셔티브에 배정했으나, 준비가 충분히 갖춰졌다고 보고한 마케팅 조직은 고작 30%에 그쳤으며, 대행사 파트너가 메워야 할 명확한 실행상의 격차가 남게 되었습니다. 이 차이가 중요한 이유는 클라이언트가 단순히 자동화만을 원하는 것이 아니라, 개인화, 미디어, 측정 기능을 하나의 서비스 구조로 통합할 수 있는 대행사를 찾고 있기 때문입니다. 퍼블리시스사는 2025년, AI를 활용한 제품 및 서비스가 5.6%의 유기적 성장에 300베이시스포인트를 기여함으로써 그 비즈니스 효과를 입증했습니다. 이는 AI 네이티브 실행이 이미 대규모 제공업체 시장 점유율 확대를 뒷받침하고 있음을 보여줍니다. 이와 같은 지출 구조의 변화로 인해 CTV 어트리뷰션이나 실시간 로열티 오케스트레이션과 같은 관련 분야의 업무도 확대되고 있으며, 리테이너 계약은 줄어들기는커녕 오히려 확대되는 추세를 보이고 있습니다. 따라서 통합 마케팅 서비스 시장에서 AI는 도구, 인재, 거버넌스, 크로스채널 실행을 단일 운영 모델로 통합할 수 있는 광고 대행사의 가치를 높이고 있습니다.

리테일 미디어와 크리에이터 커머스가 풀 퍼널 통합 수요를 주도하고 있습니다.

리테일 미디어는 더 이상 좁은 의미에서 하류 퍼널의 전술로만 취급되지 않으며, 이러한 변화로 인해 통합 마케팅 서비스 시장 전반에서 브랜드가 대행사 파트너에게 요구하는 조정 수준이 높아지고 있습니다. 덴츠는 2026년 전 세계 리테일 미디어의 성장률을 12.3%로 예측하고 있으며, 이는 가장 빠르게 성장하는 디지털 채널 중 하나로 평가되어, 쇼퍼 마케팅, 오디언스 전략, 브랜드 구축에서 리테일 미디어의 역할을 더욱 공고히 하고 있습니다. 이를 통해 대행사는 각 영역을 개별적으로 다루기보다는 소매업체의 데이터, 컨텐츠, 미디어 기획, 그리고 퍼널 업스트림 단계의 브랜드 포지셔닝을 유기적으로 연계해야 한다는 점이 시사됩니다. 퍼블리시스는 2025년에 captiv8 및 HEPMIL을 포함한 볼트온형 인수에 10억 유로(10억 8,000만 달러)를 투자함으로써, 크리에이터 인텔리전스, 인플루언서 커머스, 지역별 디지털 활성화 분야에서 입지를 확대함으로써 이러한 방향성을 한층 더 강화했습니다. 이 점이 중요한 이유는 광고 대행사가 타겟 고객에 대한 인사이트를 소매업체의 마케팅 활동과 연계하여 컨텐츠에서 구매에 이르는 경로를 완성할 수 있다면, 크리에이터 커머스의 가치가 더욱 높아지기 때문입니다. 실제로, 이로 인해 통합 마케팅 서비스 시장은 더 광범위한 고객 기반, 더 고액의 리테이너 계약, 그리고 헬스 및 뷰티와 같은 수직 시장에서의 더욱 강력한 카테고리 전문화로 나아가고 있습니다.

개인정보 보호 규제와 신호 손실로 인해 확보 가능한 도달 범위가 축소됨

개인정보 보호 규제의 시행은 더 이상 법적 검토에 그치지 않고, 통합 마케팅 서비스 시장의 캠페인 설계 및 기여도 분석에도 영향을 미치고 있습니다. 2026년 1월 기준으로, 미국 12개 주 이상의 규정에 따라 기업들은 브라우저 기반의 범용 옵트아웃 신호를 감지하고 이에 따라야 할 의무가 부과되었습니다. 이로 인해 퍼포먼스 마케팅에서 기본 추적 전제를 적용할 수 있는 실질적인 여지가 줄어들었습니다. 또한 캘리포니아주는 주 의회 법안 566호를 통해 브라우저 수준의 옵트아웃 요건을 더욱 강화함으로써, 보다 자동화되고 지속적인 동의 환경으로의 전환을 시사했습니다. 2026년 6월 구글이 발표한 '동의 모드'의 변경 사항은 EEA(유럽경제지역)의 광고주에게 GA4에서 Google Ads로 전송되는 광고 데이터를 제어할 수 있는 주요 수단을 'ad_storage'로 한정함으로써, 운영상의 부담을 더욱 가중시켰습니다. 그 결과, 일부 캠페인의 경우 대상 사용자층이 축소되었으며, 더 강력한 동의 관리와 퍼스트파티 데이터 워크플로가 필요해진 대행사 입장에서는 인프라 비용 증가로 이어지고 있습니다. 그럼에도 불구하고, 이러한 컴플라이언스 업무를 보다 광범위한 서비스 패키지에 통합할 수 있다면, 통합 마케팅 서비스 시장에서 시장 제약 요인을 고객 유지의 경쟁 우위로 전환할 수 있습니다.

부문별 분석

2025년, 광고 및 미디어 기획, 구매 서비스는 33.68%의 점유율을 차지했으며, 통합 마케팅 서비스 시장에서 가장 큰 수익원이 되었습니다. 이러한 위상은 대규모 광고 대행사의 운영 모델에서 프로그래매틱 미디어, 월드가든형 바이잉, 그리고 크로스채널 기획이 여전히 핵심적인 역할을 수행하고 있음을 반영합니다. 옴니콤의 미디어·광고 부문은 2025년에 100억 달러의 매출을 기록했으며, 이는 기업 수익의 58%를 차지했습니다. 이는 유료 미디어 및 관련 실행 서비스가 여전히 어느 정도의 규모를 차지하고 있는지를 보여줍니다. 홍보 및 커뮤니케이션 서비스 역시 여전히 중요한 위치를 차지하고 있으며, 2025년 옴니콤의 체험형 마케팅 사업이 고정 환율 기준으로 19% 성장한 것은 어닝 미디어, 컨텐츠, 이벤트, 브랜드 체험 간의 시너지 효과가 더욱 강화되고 있음을 시사합니다.

브랜드 전략 및 크리에이티브 서비스는 더욱 큰 압박에 직면해 있으며, 옴니콤의 브랜딩 및 소매 상거래 부문은 2025년 연간 기준으로 고정 환율 기준 15.8% 감소했습니다. 이는 많은 고객사가 크리에이티브 예산을 보다 광범위한 미디어 중심의 위탁 업무에 포함시키고 있음을 시사합니다. 디지털 마케팅 서비스는 2026년부터 2031년까지 연평균 성장률(CAGR) 7.21%로 확대될 것으로 예상되며, 통합 마케팅 서비스 업계에서 가장 빠르게 성장하는 서비스 분야가 될 것입니다. 이러한 성장은 검색, 소셜 커머스, 커넥티드 TV, 생성형 AI를 통한 엔진 최적화에 대한 수요 증가를 반영한 것으로, 이 모든 분야는 더 신속한 테스트, 더 많은 데이터 피드백, 그리고 컨텐츠와 미디어 간의 더욱 긴밀한 연계를 필요로 합니다. 컨텐츠 및 캠페인 관리 서비스는 물론, 고객 참여, CRM, 로열티 서비스도 브랜드들이 자사 보유 데이터, 캠페인 실행, 고객 유지 프로그램을 단일 서비스 구조 내에서 통합할 수 있도록 지원하는 대행사의 도움을 필요로 하고 있어 성장세를 보이고 있습니다. ISO 27001, GDPR(EU 개인정보보호규정), CCPA 준수 등 규정 준수 기준도 조달 시 선정 기준으로 자리 잡고 있으며, 이는 통합 마케팅 서비스 시장에서 서비스의 차별화가 크리에이티브 및 미디어 역량과 마찬가지로 운영상의 보증에 달려 있음을 의미합니다.

2025년에는 리테이너형 계약이 총 수익의 41.48%를 차지했으며, 통합 마케팅 서비스 시장의 주요 제공 모델이 되었습니다. 기업의 마케팅 담당자들은 여전히 지속성, 체계적인 인사이트, 그리고 여러 시장과 기능에 걸친 협력을 중시하고 있기 때문에 이러한 구조가 지배적인 위치를 유지하고 있습니다. 대규모 고객은 미디어, 데이터, CRM, 크리에이티브 활동을 단일한 공유된 운영 리듬에 따라 진행해야 할 경우, 종종 장기적인 관계에 의존하는 경향이 있습니다. 하이네켄의 2025년 파트너 선정은 이러한 패턴을 여실히 보여주고 있습니다. 이 회사는 전 세계 미디어 업무를 담당할 업체로 덴츠를 재선정하고, 크리에이티브 업무는 퍼블리시스, 스태그웰, WPP에 분산시켰습니다. 이는 고객사가 파트너를 다각화한 경우에도, 핵심이 되는 통합 업무에 대해서는 안정적인 장기적 관계를 지속적으로 유지하고 있음을 보여줍니다.

프로젝트 기반 계약이나 하이브리드형 임베디드 팀을 통한 계약이 확대되고 있는 것은 중견 시장 고객사의 상당수가 처음부터 광범위한 다년 계약을 체결하지 않고 유연성을 추구하기 때문입니다. 하이브리드형 구조는 브랜드가 사내 AI 역량을 구축해 나가면서도, 실행, 통합, 인재 지원 측면에서 여전히 대행사의 지원이 필요한 경우에 특히 효과적입니다. 퍼블리시스는 마르셀(Marcel) 및 관련 임베디드 인재 인프라를 통해 이 모델에 주력하고 있으며, 이를 통해 클라이언트의 사내 팀과 대행사의 전문가 간의 협업 체제가 뒷받침되고 있습니다. 성과 연계형 계약은 2031년까지 연평균 성장률(CAGR) 8.02%를 나타낼 것으로 예측되며, 이는 어트리뷰션이 개선됨에 따라 구매자들이 성과 연계형 가격 책정을 얼마나 강력하게 선호하게 되었는지를 보여줍니다. 통합 마케팅 서비스 업계에 있어 이는 이점과 위험을 동시에 가져옵니다. 왜냐하면, 대행사는 초기 성과를 거둔 후 클라이언트와의 관계를 심화시킬 수 있는 반면, 측정 결과가 보수의 기준이 됨으로써 더 큰 위험을 감수하게 되기 때문입니다.

지역별 분석

북미는 2025년에 통합 마케팅 서비스 시장 점유율의 34.46%를 차지했으며, 2026년에도 여전히 최대 지역 시장으로 자리매김했습니다. 이 지역은 기업 광고 예산이 가장 집중되어 있고, 가장 성숙한 프로그래매틱 인프라를 갖추고 있으며, 세계 최대의 지주회사 본사가 위치해 있다는 등의 장점을 가지고 있습니다. 옴니콤은 2025년 미국 사업에서 91억 달러의 매출을 올렸으며, 이는 해당 기업의 총 매출의 52.7%를 차지해 이 시장에 집중된 수요의 규모를 여실히 보여주고 있습니다. 퍼블리시스 역시 2025년 북미에서 5.4%의 유기적 성장을 기록했으며, 미국이 그룹 순매출의 57%를 차지하고 있는 점은 전 세계 광고 대행사의 실적에서 해당 지역이 구조적으로 중요한 위치를 차지하고 있음을 뒷받침합니다. 동시에 미국 시장에서는 개인정보 보호 규제가 강화되고 있으며, 이에 따라 광고 예산이 퍼스트파티 데이터와 연계된 채널로 이동하고 있어, 규정 준수 및 활성화(activation)를 통합적으로 관리할 수 있는 통합 서비스 모델의 가치가 높아지고 있습니다.

유럽은 ‘디지털 우선’ 미디어 투자와 성숙한 국경을 초월한 브랜드 활동에 힘입어, 통합 마케팅 서비스 시장에서 여전히 2위 지역 블록으로서의 위상을 유지했습니다. 퍼블리시스는 2025년 유럽의 유기적 성장률을 4.2%로 보고했으며, 독일은 8.9%, 영국은 7.2%를 기록했습니다. 이는 규제 환경이 강화되고 있음에도 불구하고 수요가 견조한 추세를 보이고 있음을 보여줍니다. GDPR(EU 개인정보보호규정), 디지털 서비스법, AI법으로 인해 규정 준수 비용이 증가하고 있으며, 이에 따라 거버넌스 비용을 보다 광범위한 고객 포트폴리오에 분산시킬 수 있는 대형 네트워크 기업들이 우위를 점하고 있습니다. 남미는 절대 규모 면에서는 여전히 작은 편이지만, 2025년에는 강력한 성장세를 보였으며, 옴니콤의 지역 매출은 고정 환율 기준으로 29.3% 증가했고, 퍼블리시스도 18.7%의 유기적 성장을 기록했습니다. 이러한 개선을 주도한 것은 브라질과 아르헨티나였습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.20%를 나타낼 것으로 예측되며, 통합 마케팅 서비스 시장에서 가장 빠르게 성장하는 지역이 될 것입니다. 이 지역은 디지털 광고 인프라의 강화, 소매 미디어의 급속한 확대, 그리고 연결된 사용자 여정 속에서 상거래, 결제, 컨텐츠를 뒷받침하는 플랫폼 생태계로부터 혜택을 받고 있습니다. 제출된 초안에서는 2026년 인도의 디지털 광고 지출이 9.6% 증가할 것으로 전망되며, 호주, 중국, 일본, 인도 전역에서 소매 미디어의 확대가 가속화되고 있는 점도 지적되고 있는데, 이러한 요인들이 해당 지역의 성장세를 뒷받침하고 있습니다. 또한, 슈퍼 앱이나 마켓플레이스 환경 덕분에 노출, 거래, 측정 간의 프로세스가 단축됨에 따라 동남아시아의 커머스·미디어 모델의 중요성도 높아지고 있습니다. 아시아태평양 이외의 지역 중에서는 중동이 2025년에 10.8%라는 퍼블리시스 포트폴리오 내에서 가장 높은 집중적인 유기적 성장을 기록했습니다. 이는 사우디아라비아와 UAE에서의 지속적인 브랜드 투자를 반영한 것입니다. 아프리카는 매출액 기준으로 여전히 가장 작은 지역이지만, 남아프리카공화국, 나이지리아, 이집트에서의 '모바일 우선'의 보급으로 인해 현지 브랜드의 규모 확대와 다국적 기업의 사업 범위 확대에 따라, 보다 종합적인 에이전시 기능에 대한 초기 수요가 뒷받침되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the integrated marketing services market size is expected to increase from USD 398.91 billion in 2025 to USD 425.73 billion in 2026 and reach USD 595.56 billion by 2031, growing at a CAGR of 6.94% over 2026-2031.

This report is Segmented by Service Type (Brand Strategy and Creative Services, Digital Marketing Services, and More), Delivery Model (Project-Based Engagement, Retainer-Based Engagement, and More), Organization Size (Small and Medium-Sized Enterprises, and More), End-User Industry (Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD)

Global Integrated Marketing Services Market Trends and Insights

Artificial Intelligence-Enabled Personalization Reshapes Agency Value Proposition

Artificial intelligence is reducing the time between audience analysis and live campaign delivery, and that shift is changing the commercial model of the integrated marketing services market. In 2026, CMOs allocated 15.3% of total marketing budgets to AI initiatives, yet only 30% of marketing organizations reported mature readiness, which left a clear execution gap for agency partners to fill. That gap matters because clients are not only looking for automation, they are also looking for agencies that can connect personalization, media, and measurement into one service structure. Publicis showed the commercial effect in 2025, when AI-powered products and services contributed 300 basis points to its 5.6% organic growth, which indicates that AI-native execution is already supporting share gains for scaled providers. The same spending shift is expanding work in adjacent areas such as CTV attribution and real-time loyalty orchestration, so retainers are becoming broader rather than smaller. For the integrated marketing services market, AI is therefore raising the value of agencies that can combine tools, talent, governance, and cross-channel execution in one operating model.

Retail Media and Creator Commerce Drive Demand for Full-Funnel Integration

Retail media is no longer treated as a narrow lower-funnel tactic, and that shift is increasing the amount of coordination brands expect from agency partners across the integrated marketing services market. Dentsu projected global retail media growth of 12.3% in 2026, which placed it among the fastest-growing digital channels and reinforced its role in shopper marketing, audience strategy, and brand building.The implication is that agencies now need to connect retailer data, content, media planning, and upper-funnel brand positioning instead of handling each area separately. Publicis reinforced that direction in 2025 by investing EUR 1 billion (USD 1.08 billion) in bolt-on acquisitions that included captiv8 and HEPMIL, which expanded its position in creator intelligence, influencer commerce, and regional digital activation. This matters because creator commerce is becoming more valuable when agencies can link audience insight to retailer activation and close the path from content to purchase. In practice, that is pushing the integrated marketing services market toward broader account scopes, larger retainers, and stronger category specialization in verticals such as health and beauty.

Privacy Regulation and Signal Loss Compress Addressable Reach

Privacy enforcement is now affecting campaign design and attribution inside the integrated marketing services market, not just legal review. As of January 2026, rules across 12 or more U.S. states required businesses to detect and honor browser-based universal opt-out signals, which reduced the practical room for default tracking assumptions in performance marketing. California also moved browser-level opt-out requirements further forward through Assembly Bill 566, which signaled a more automated and persistent consent environment. Google's June 2026 Consent Mode change added another layer of operational pressure by making ad_storage the main control over what ad data passes from GA4 into Google Ads for EEA advertisers. The result is a smaller addressable pool for some campaigns and higher infrastructure costs for agencies that now need stronger consent management and first-party data workflows. Even so, agencies that absorb those compliance tasks into broader service bundles can turn a market restraint into a client retention advantage within the integrated marketing services market.

Other drivers and restraints analyzed in the detailed report include:

- First-Party Data and Clean-Room Adoption Create Long-Cycle Agency Dependency

- Performance-Based Contracts Redefine Integrated Agency Pricing Architecture

- Generative Artificial Intelligence Rights and Indemnity Exposure Elevate Agency Liability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Advertising and Media Planning and Buying Services held 33.68% share in 2025, which made it the largest revenue block in the integrated marketing services market. That position reflects the continuing central role of programmatic media, walled-garden buying, and cross-channel planning in large agency operating models. Omnicom's Media and Advertising discipline generated USD 10 billion in 2025, or 58% of total company revenue, which showed how much scale still sits inside paid media and related execution services. Public Relations and Communications Services remained relevant because experiential work expanded 19% in constant currency for Omnicom in 2025, which pointed to a stronger overlap between earned media, content, events, and brand experience.

Brand Strategy and Creative Services faced more pressure, and Omnicom's Branding and Retail Commerce discipline declined 15.8% in constant currency in full-year 2025, which suggested that many clients were folding creative budgets into wider media-led mandates. Digital Marketing Services is projected to advance at a 7.21% CAGR from 2026 to 2031, which makes it the fastest-growing service area in the integrated marketing services industry. Its growth reflects stronger demand for search, social commerce, connected TV, and generative engine optimization, all of which require faster testing, more data feedback, and tighter links between content and media. Content and Campaign Management Services, along with Customer Engagement, CRM and Loyalty Services, are also moving upward because brands want agency support that connects owned data, campaign activation, and retention programs inside one service structure. Compliance markers such as ISO 27001 and GDPR or CCPA readiness are becoming procurement filters as well, which means service differentiation now depends on operational assurance as much as creative or media capability in the integrated marketing services market.

Retainer-Based Engagement accounted for 41.48% of total revenue in 2025, which made it the leading delivery model in the integrated marketing services market. This structure remains dominant because enterprise marketers still value continuity, institutional knowledge, and coordination across multiple markets and functions. Large accounts often rely on long-duration relationships when media, data, CRM, and creative activity need to move through one shared operating rhythm. Heineken's 2025 roster decision illustrated that pattern, because the company reappointed Dentsu for global media and distributed creative work across Publicis, Stagwell, and WPP, which showed that even when clients diversify partners, they still preserve stable long-term relationships for core integrated work.

Project-Based Engagement and Hybrid Embedded Team Engagement are expanding because more mid-market clients want flexibility without signing broad multi-year agreements at the start. Hybrid structures are especially relevant when brands are building internal AI capabilities and still need agency help for execution, integration, and talent support. Publicis has leaned into that model through Marcel and related embedded talent infrastructure, which supports co-working arrangements between internal client teams and agency specialists. Performance-Based Engagement is projected to grow at a 8.02% CAGR through 2031, which shows how strongly buyers now favor outcome-linked pricing once attribution improves. For the integrated marketing services industry, that creates both upside and risk, because agencies can deepen client relationships after early performance wins, but they also take on more exposure when measurement becomes the basis for compensation.

Complete Report Scope:

- By Service Type

- Brand Strategy and Creative Services

- Advertising and Media Planning and Buying Services

- Digital Marketing Services

- Public Relations and Communications Services

- Content and Campaign Management Services

- Customer Engagement, Customer Relationship Management and Loyalty Services

- Other Service Types

- By Delivery Model

- Project-Based Engagement

- Retainer-Based Engagement

- Performance-Based Engagement

- Hybrid and Embedded Team Engagement

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-User Industry

- Retail and E-commerce

- Consumer Goods and Beauty

- Media and Entertainment

- IT and Telecom

- BFSI

- Healthcare and Life Sciences

- Other End-User Industries (Education, Travel and Hospitality, Industrial, Automotive)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 34.46% of the integrated marketing services market share in 2025, and it remained the largest regional base in 2026. The region benefits from the deepest concentration of enterprise advertising budgets, the most mature programmatic infrastructure, and the headquarters presence of the largest global holding companies. Omnicom generated USD 9.1 billion from U.S. operations in 2025, or 52.7% of total company revenue, which illustrated the scale of demand concentrated in this market. Publicis also reported 5.4% organic growth in North America in 2025, with the United States contributing 57% of the group's net revenue, which confirmed the region's structural weight in global agency performance. At the same time, the U.S. market is dealing with tighter privacy enforcement, which is pushing spend toward first-party-data-connected channels and raising the value of integrated service models that can manage compliance and activation together.

Europe remained the second-largest regional block in the integrated marketing services market, supported by digital-first media investment and mature cross-border brand activity. Publicis reported 4.2% organic growth in Europe in 2025, with Germany at 8.9% and the United Kingdom at 7.2%, which showed that demand remained healthy despite a stricter regulatory setting. GDPR, the Digital Services Act, and the AI Act are increasing compliance costs, and that is giving larger networks an advantage because they can spread governance costs across wider client portfolios. South America remained smaller in absolute size, but growth was strong in 2025 as Omnicom's regional revenue rose 29.3% in constant currency and Publicis reported 18.7% organic growth, with Brazil and Argentina leading the improvement.

Asia-Pacific is projected to grow at an 8.20% CAGR through 2031, which makes it the fastest-growing geography in the integrated marketing services market size. The region is benefiting from stronger digital ad infrastructure, rapid retail media expansion, and platform ecosystems that support commerce, payments, and content inside connected user journeys. The supplied draft also pointed to 9.6% digital ad spending growth in India in 2026 and stronger retail media expansion across Australia, China, Japan, and India, which supports the region's faster momentum. Southeast Asia's commerce-media model is also becoming more important because super-app and marketplace environments are shortening the path between exposure, transaction, and measurement. Outside Asia-Pacific, the Middle East posted the strongest concentrated organic growth inside Publicis's portfolio at 10.8% in 2025, which reflected continued brand investment in Saudi Arabia and the UAE. Africa remained the smallest geography by revenue, but mobile-first adoption in South Africa, Nigeria, and Egypt is supporting early demand for fuller agency capabilities as local brands scale and multinationals expand coverage.

- Omnicom Group Inc.

- Publicis Groupe S.A.

- WPP plc

- Dentsu Group Inc.

- Accenture plc

- Havas N.V.

- Stagwell Inc.

- Deloitte Touche Tohmatsu Limited

- Capgemini SE

- Cognizant Technology Solutions Corporation

- Tata Consultancy Services Limited

- Infosys Limited

- Hakuhodo DY Holdings Inc.

- BlueFocus Intelligent Communications Group Co., Ltd.

- Daniel J. Edelman Holdings, Inc.

- Ruder Finn, Inc.

- FINN Partners, Inc.

- LLYC S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Omnichannel Brand Consistency Mandates

- 4.2.2 Performance-Based Budget Allocation

- 4.2.3 Artificial Intelligence-Enabled Personalization and Content Production

- 4.2.4 Retail Media and Creator Commerce Expansion

- 4.2.5 First-Party Data Collaboration and Clean-Room Adoption

- 4.2.6 Fragmented Small and Medium-Sized Business Martech Stacks Increasing Agency Outsourcing

- 4.3 Market Restraints

- 4.3.1 Privacy Regulation and Signal Loss

- 4.3.2 Cross-Channel Measurement Fragmentation

- 4.3.3 Generative Artificial Intelligence Rights and Indemnity Exposure

- 4.3.4 Answer-Engine Search and Platform Volatility

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Brand Strategy and Creative Services

- 5.1.2 Advertising and Media Planning and Buying Services

- 5.1.3 Digital Marketing Services

- 5.1.4 Public Relations and Communications Services

- 5.1.5 Content and Campaign Management Services

- 5.1.6 Customer Engagement, Customer Relationship Management and Loyalty Services

- 5.1.7 Other Service Types

- 5.2 By Delivery Model

- 5.2.1 Project-Based Engagement

- 5.2.2 Retainer-Based Engagement

- 5.2.3 Performance-Based Engagement

- 5.2.4 Hybrid and Embedded Team Engagement

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 Retail and E-commerce

- 5.4.2 Consumer Goods and Beauty

- 5.4.3 Media and Entertainment

- 5.4.4 IT and Telecom

- 5.4.5 BFSI

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Other End-User Industries (Education, Travel and Hospitality, Industrial, Automotive)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Qatar

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Omnicom Group Inc.

- 6.4.2 Publicis Groupe S.A.

- 6.4.3 WPP plc

- 6.4.4 Dentsu Group Inc.

- 6.4.5 Accenture plc

- 6.4.6 Havas N.V.

- 6.4.7 Stagwell Inc.

- 6.4.8 Deloitte Touche Tohmatsu Limited

- 6.4.9 Capgemini SE

- 6.4.10 Cognizant Technology Solutions Corporation

- 6.4.11 Tata Consultancy Services Limited

- 6.4.12 Infosys Limited

- 6.4.13 Hakuhodo DY Holdings Inc.

- 6.4.14 BlueFocus Intelligent Communications Group Co., Ltd.

- 6.4.15 Daniel J. Edelman Holdings, Inc.

- 6.4.16 Ruder Finn, Inc.

- 6.4.17 FINN Partners, Inc.

- 6.4.18 LLYC S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment