|

시장보고서

상품코드

1683932

아시아태평양의 자동차용 LED 조명 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Asia Pacific Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

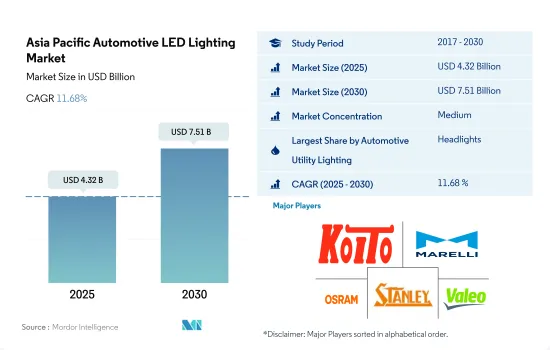

아시아태평양의 자동차용 LED 조명 시장 규모는 2025년에 43억 2,000만 달러에 달할 것으로 추정됩니다. 2030년에는 75억 1,000만 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년) CAGR은 11.68%를 나타낼 것으로 전망됩니다.

아시아태평양에서 사고 삭감을 목적으로 한 자동차 LED 조명 기술 혁신이 진행되어 시장 수요 견인

- 금액 점유율에서는 2022년 전조등 시장의 대부분을 차지한 다음 그 밖에 방향지시등이 이어졌습니다. 예측 기간 동안 방향지시등과 정지 램프 시장 점유율은 거의 동일하며 전조등의 변동은 작을 것으로 예상됩니다. 중국은 자동차 부품 제조의 주요 국가이며 예측 기간 동안에도 우위를 유지할 것으로 예상됩니다.

- 수량 점유율에서 2022년에는 방향지시등이 대부분을 차지한 다음 전조등이 되었습니다. 이러한 조명 시장 점유율은 변동이 적고 앞으로도 변하지 않을 것으로 예상됩니다. Tata, Hyundai, SAIC, Geely는 향후 자동차에 LED 프로젝터 라이트를 장착하는 몇 가지 주요 기업입니다. 사고율이 증가함에 따라 LED 안개등이 널리 보급될 것으로 예상됩니다. 중국, 인도, 일본 등의 국가들은 LED 램프를 자동차에 채용함으로써 사고율을 낮추고 있습니다. 예를 들어 2017년에는 총 4,64,910건의 교통사고가 발생했으나 2021년에는 4,12,432건까지 감소했습니다. 이와 같이 차량에 LED 램프를 사용함으로써 각국의 교통사고로 인한 사상자 수를 줄일 것으로 기대됩니다.

- 또한 LED는 자동차의 외관을 향상시키는 혁신적인 조명 개념 개발에도 기여하고 있습니다. 각 기업은 협력하여 자동차 산업용 기술 LED 제품을 개발하고 있습니다. 예를 들어, 2022년 9월, ams 오스람과 TactoTek은 아방가르드 OSIRE E5515 사이드 뷰 RGB LED가 장착된 시연자 개발에 협업을 발표했습니다. 차실내에 간단하게 짜넣을 수 있어 보다 컴팩트한 디자인이 됩니다. 자동차 LED 조명에 대한 이러한 혁신과 미래 투자는 예측 기간 동안 시장을 견인할 것으로 예상됩니다.

한국, 중국, 인도 및 기타 아시아태평양의 주요 국가에서 EV의 성장이 LED 조명 판매를 밀어 올릴 것으로 보입니다.

- 금액 점유율에서는 2022년 아시아태평양의 자동차용 LED 조명 시장에서 중국이 대부분의 점유율을 차지했고 일본, 인도가 그 뒤를 이었습니다. 중국 시장 점유율은 2030년에 제조업 부문의 성장과 전국 자동차 산업의 기술 혁신 증가에 따라 증가할 것으로 예상됩니다. 인도 시장 점유율도 국내 자동차 기업의 대부분이 EV에 투자하고 있으며, EV 성장을 지원하는 정부의 이니셔티브도 높아지고 있기 때문에 확대가 예상됩니다.

- 대수 점유율에서는 중국이 2022년 시장 점유율의 대부분을 차지했고 인도, 일본 및 기타 아시아태평양이 뒤를 이었습니다. 한국은 수량 점유율에서 가장 낮고 예측기간을 통해 소수파에 머물 것으로 예상됩니다. 중국은 세계 기타 지역의 수출입 허브이며 주요 반도체 제조업이 위치하고 있습니다. 2019년 중국은 2,600만 대 이상의 자동차를 생산했으며 대부분은 각국에 수출되었습니다.

- 한국에서는 2022년 판매량이 2021년에 비해 감소했습니다. 이는 지정학적 문제로 중국과 러시아에서의 판매가 약해졌기 때문입니다. 그러나 이 나라에서는 EV를 추진하는 정부 자회사가 증가하고 있으며, EV 자동차 산업은 향후 수년간 성장할 것으로 예상됩니다.

- 2021년 전기차 판매량 증가는 주로 중국이 견인하고 성장의 절반을 차지했습니다. 이와 같이 EV전체의 성장은 LED기술 혁신 증가와 물류부문의 성장과 함께 자동차산업에서의 LED전체의 성장을 세계적으로 높일 것으로 예상됩니다.

아시아태평양의 자동차용 LED 조명 시장 동향

더 많은 전기자동차 판매를 위한 EV 인센티브 증가는 LED 시장 성장을 견인

- 아시아태평양의 자동차 총 생산량은 2022년에는 1억 429만대였으며, 2023년에는 1억 965만대에 달했습니다. COVID-19의 유행은 아시아태평양의 자동차 시장에 큰 영향을 미쳤습니다. 예를 들어 2019년 3월에 비해 뉴질랜드의 자동차 및 상용차 판매 대수는 37% 감소했습니다. 2020년 3월 23일에는 혼다나 인더스 모터 등 자동차 제조업체가 파키스탄에서의 생산을 정지했습니다. 나머지 아시아태평양 국가들도 비슷한 상황에 빠졌습니다. 그 결과 COVID-19 팬데믹 동안 자동차 산업의 LED 수요는 전반적으로 감소했습니다.

- TATA Motors, Mahindra & Mahindra, SAIC Motor, 吉利汽車, 長城汽車, 奇瑞汽車, 도요타 등이 이 지역의 주요 자동차 제조 업체입니다. 이 모든 기업들은 EV 생산에 주력하고 있습니다. 아시아태평양에서는 자동차 기술 혁신이 급속히 진행되고 있으며, 2022년에는 중국에서만 세계 EV 판매 대수의 약 65%를 차지했습니다. LED는 효율성으로 인해 EV에서의 사용이 증가할 것으로 예측됩니다. 예를 들어, EV에 LED를 탑재하면 배터리의 소비 전류가 줄어들기 때문에 한 번의 충전으로 항속 거리가 6마일 늘어날 수 있습니다.

- 전기자동차(EV)는 내연 엔진 대신 전기 모터가 장착된 자동차이며 LED 자동차 조명과 호환됩니다. 환경에 대한 이점, 실행 비용 절감, 기술 발전으로 EV는 이 지역에서 성장하고 있습니다. LED 자동차 조명은 최대 10,000시간까지 사용할 수 있으므로 환경에 미치는 영향을 줄일 수 있습니다. 자동차 산업에서 LED 조명의 많은 장점으로 인해 LED 수요와 성장은 예상되는 기간에 증가할 것으로 보입니다.

배터리 교환 스테이션, 배터리 리사이클 서비스 점포, EV 보조금의 급성장이 LED 시장을 견인

- 아시아태평양 최대 자동차 시장인 중국은 고성능 EV의 지역 최대 시장이며 그 뒤를 잇는 건 일본입니다. 아시아태평양의 배기 가스 규제와 하이브리드 자동차 및 전기자동차에 대한 보조금은 전기자동차 및 하이브리드 자동차 시장 전체의 상당한 점유율을 얻는 데 도움이되었습니다. 중국에는 2022년 말 시점에 EV 충전소이 약 160만 곳, 충전 포인트가 521만 곳(2022년에 건설된 259만 곳 이상 포함)이 있었습니다. 중국은 10년 이상 소비자에 대한 까다로운 인센티브와 자동차 제조업체에 대한 보조금으로 EV 산업을 추진해 왔습니다. 예를 들어, EV 구매자는 약 60,000 위안의 할인을 받았지만 2022년에 종료되었습니다.

- 2022년 기준 일본에는 28,546곳의 충전소가 있었습니다. 2022년도 일본에서 판매된 수입전기자동차의 대수는 전년대비 65% 증가한 1만6,464대로 과거 최고를 기록했습니다. 일본에서 새롭게 판매된 승용차는 361만대로, 2022년도 중에 약 7만7,000대가 EV였습니다. 인도에서는 2023년 3월까지 6586곳의 공공 충전소(PCS)이 가동되었습니다. 또한 정부는 FAME-II, PLI SCHEME, 배터리 스위칭 정책, EV 감세 등의 자본 보조금을 제공함으로써 EV 충전소의 설치를 촉진하고 있습니다. 2019년 4월에는 50만대의 E-3륜차, 7,000대의 E-버스, 5만 5,000대의 E-승용차, 100만대의 E-이륜차를 지원하기 위해 10,000캐롤 루피(12억 달러)의 예산으로 FAME II 계획이 도입되었습니다. 그 목적은 인도에서 전기자동차의 보급을 촉진하는 것이 었습니다. 이 계획은 2022년에 종료될 예정이었습니다. 이와 같이 위의 사례는 개발도상국 전체의 EV 수요 증가에 따른 새로운 발전소의 개발과 생산으로 이어져 자동차용 LED 수요를 끌어올립니다.

아시아태평양의 자동차용 LED 조명 산업 개요

아시아태평양의 자동차용 LED 조명 시장은 적당히 통합되어 상위 5개사에서 56.82%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. KOITO MANUFACTURING, Marelli Holdings, OSRAM GmbH., Stanley Electric and Valeo(알파벳순 정렬).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 자동차 생산 대수

- 인구

- 1인당 소득

- 자동차 대출 금리

- 충전소 수

- 자동차 보유 대수

- 총 수입량

- 가구수

- 도로 네트워크

- LED 보급률

- 규제 프레임워크

- 중국

- 인도

- 일본

- 한국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 자동차용 유틸리티 조명

- 주간 주행등(DRL)

- 방향지시등

- 전조등

- 후진등

- 정지등

- 후미등

- 기타

- 자동차용 조명

- 이륜차

- 상용차

- 승용차

- 국가

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

- GRUPO ANTOLIN IRAUSA, SA

- HELLA GmbH & Co. KGaA(FORVIA)

- Hyundai Mobis

- KOITO MANUFACTURING CO., LTD.

- Marelli Holdings Co., Ltd.

- Nichia Corporation

- OSRAM GmbH.

- Stanley Electric Co., Ltd.

- Uno Minda Limited

- Valeo

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Asia Pacific Automotive LED Lighting Market size is estimated at 4.32 billion USD in 2025, and is expected to reach 7.51 billion USD by 2030, growing at a CAGR of 11.68% during the forecast period (2025-2030).

Increasing innovations in LED lighting in automobiles to reduce accidents in Asia-Pacific drive the market demand

- In terms of value share, in 2022, headlights accounted for the majority of the market, followed by others and directional signal lights. The market share is expected to remain almost the same for directional signal lights and stop lights during the forecast period, with a small variation in headlights. China is the major country in terms of manufacturing automotive components, and it is expected to maintain its dominance over the forecasted period.

- In terms of volume share, in 2022, directional signal lights accounted for the majority, followed by headlights and others. The market share is expected to remain the same with less fluctuation for these lights. Tata, Hyundai, SAIC, and Geely are among the few major companies incorporating LED projector lights in their upcoming vehicles. As the accident rate rises, LED fog lamps are expected to become more popular. Countries such as China, India, and Japan have reduced accident rates by using LED lamps in their vehicles. For example, there were a total of 4,64,910 traffic accidents in 2017, but it dropped to 4,12,432 in 2021. Thus, using LED lamps in vehicles is expected to reduce the number of casualties in traffic accidents in countries.

- In addition, LEDs contribute to developing innovative lighting concepts that enhance the appearance of vehicles. Companies work together to develop technical LED products for the automotive industry. For example, in September 2022, ams OSRAM and TactoTek announced their collaboration on the development of a demonstrator featuring the avant-garde OSIRE E5515 side-view RGB LED. It can be easily integrated into the car interior, resulting in a more compact design. Such innovations and future investments in automotive LED lighting are expected to drive the market during the forecast period.

The growth of EVs in South Korea, China, India, and other major countries in Asia-Pacific would boost the sales of LED lights

- In terms of value share, China accounted for the majority of the share of the Asia-Pacific automotive LED lighting market in 2022, followed by Japan and India. The market share is expected to increase for China in 2030 owing to the growth in the manufacturing sector and increasing innovation in automotive industries across the country. The market share of India is also expected to increase as the majority of automotive companies in the country are investing in EVs, and government initiatives to support the growth of EVs are also rising.

- In terms of volume share, China accounted for the majority of the market share in 2022, followed by India, Japan, and the Rest of Asia-Pacific. South Korea has the least volume share, and it is expected to remain in the minority throughout the forecast period. China is the export and import hub for the rest of the world, and major semiconductor manufacturing industries are located in the country. In 2019, China produced more than 26 million vehicles, and the majority of the vehicles were exported to various countries.

- In South Korea, sales were down in 2022 compared to 2021. This was due to weaker sales in China and Russia due to geopolitical issues. However, with rising government subsidiaries to promote EVs in the country, the EV automotive industry is expected to grow in the coming years.

- The increase in electric vehicle sales in 2021 was primarily driven by China, which accounted for half of the growth. Thus, overall EV growth, with rising LED innovation and a growing logistical sector, is expected to increase overall LED growth globally in the automotive industry.

Asia Pacific Automotive LED Lighting Market Trends

Increasing EV incentives to sell more electric vehicles to drive the growth of the LED market

- The total automobile vehicle production in Asia-Pacific was 104.29 million units in 2022, and it was expected to reach 109.65 million units in 2023. The COVID-19 pandemic had a significant effect on the Asia-Pacific automotive market. For instance, compared to March 2019, automotive and commercial vehicle sales in New Zealand were down by 37%. On March 23, 2020, automakers like Honda and Indus Motor stopped producing in Pakistan. The remainder of the Asia-Pacific nations experienced a similar situation. As a result, during the COVID-19 pandemic, the overall demand for LEDs in the automobile industry decreased.

- TATA Motors, Mahindra & Mahindra, SAIC Motor, Geely, Great Wall Motor, Chery, Toyota, and others are major automotive manufacturers in the region. All these companies are increasing their focus on the production of EVs. In Asia-Pacific, automotive innovations are growing rapidly, with China alone expected to account for around 65% of global EV sales in 2022. Due to their efficiency, LEDs are projected to be used more in EVs. For example, when LEDs are fitted on an EV, the decrease in battery current consumption can enhance range by as much as six miles on a single charge.

- Electric vehicles (EVs), automobiles with electric motors instead of internal combustion engines, are compatible with LED car lighting. Due to advantages for the environment, lower running costs, and technological advancements, EVs are growing in the region. Since LED car lights can last up to 10,000 hours, they can reduce environmental impact. The demand for and growth of LEDs will increase in the anticipated term due to the numerous advantages of LED lights in the automobile industry.

Rapid growth of battery swapping station, battery recycling service outlets, and EV subsidies are driving the LED market

- China, the region's largest automobile market, is also the region's largest market for high-performance EVs, followed by Japan. The Asia-Pacific region's emission regulations and subsidies for hybrid and electric vehicles aided it in capturing a sizable share of the overall electric and hybrid vehicle market. China had around 1.6 million EV charging stations and 5.21 million charging points at the end of 2022, including over 2.59 million that were built in 2022. China has been promoting its EV industry for more than a decade with generous incentives to consumers and subsidies to automakers. For instance, buyers received discounts of around CNY 60,000 at one point for purchasing EVs, but those ended in 2022.

- As of 2022, there were 28,546 charging stations in Japan. The number of imported electric vehicles sold in Japan during FY 2022 rose 65% from a year earlier to a record 16,464 units. There were 3.61 million passenger cars newly sold in Japan, and about 77,000 were EVs during FY 2022. By March 2023, there were 6586 public charging stations (PCS) operational in India. Furthermore, the government is promoting the installation of EV charging stations by providing capital subsidies, including FAME-II, PLI SCHEME, Battery Switching Policy, and Tax Reduction on EVs. In April 2019, the FAME II plan was introduced with an INR 10,000 crore (USD 1.2 billion) budget to support 500,000 e-three-wheelers, 7,000 e-buses, 55,000 e-passenger vehicles, and a million e-two-wheelers. The purpose was to encourage electric vehicle adoption in India. The plan was supposed to end in 2022. Thus, the above instances lead to the development and production of new power stations due to the growing demand for EVs across developing nations, which boosts the demand for automotive LEDs.

Asia Pacific Automotive LED Lighting Industry Overview

The Asia Pacific Automotive LED Lighting Market is moderately consolidated, with the top five companies occupying 56.82%. The major players in this market are KOITO MANUFACTURING CO., LTD., Marelli Holdings Co., Ltd., OSRAM GmbH., Stanley Electric Co., Ltd. and Valeo (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 China

- 4.11.2 India

- 4.11.3 Japan

- 4.11.4 South Korea

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

- 5.3 Country

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 GRUPO ANTOLIN IRAUSA, S.A.

- 6.4.2 HELLA GmbH & Co. KGaA (FORVIA)

- 6.4.3 Hyundai Mobis

- 6.4.4 KOITO MANUFACTURING CO., LTD.

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Nichia Corporation

- 6.4.7 OSRAM GmbH.

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Uno Minda Limited

- 6.4.10 Valeo

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms