|

시장보고서

상품코드

2072663

유럽의 카톤 보드 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

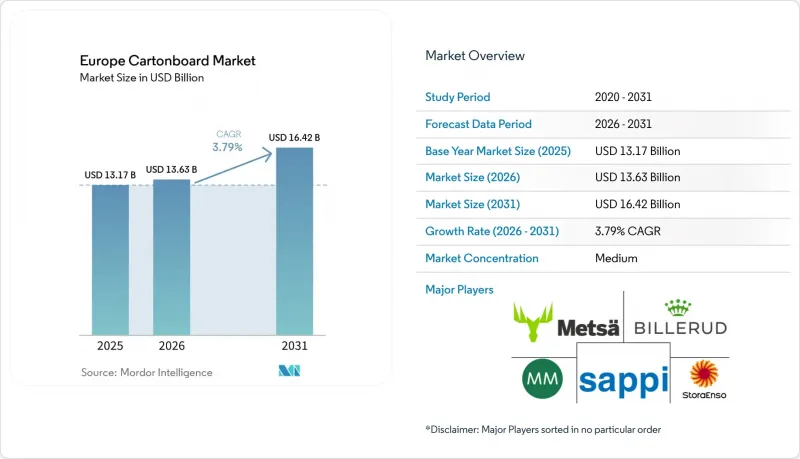

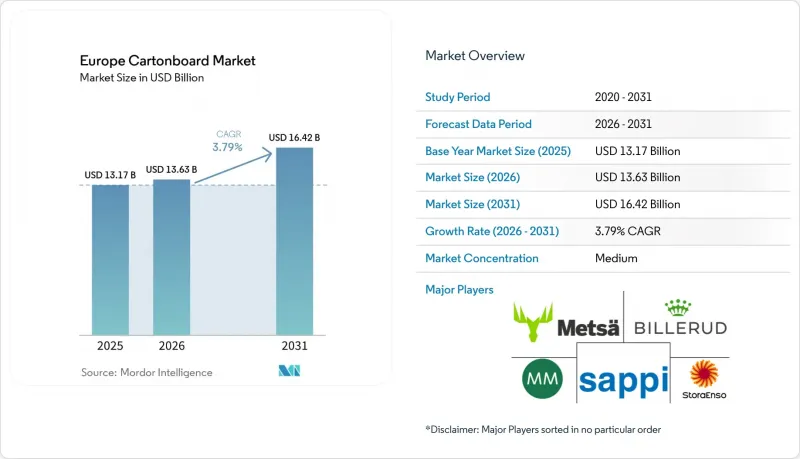

Mordor Intelligence에 의하면, 유럽의 카톤 보드 시장 규모는 2025년에 131억 7,000만 달러로 평가되었고, 2026년에 136억 3,000만 달러로 추정되고, 2031년까지 164억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 3.79%로 성장할 전망입니다.

본 보고서는 제품 등급별(솔리드 표백카톤 보드, 솔리드 미표백카톤 보드, 접이식 상자용 카톤 보드, 화이트 라이닝 칩보드, 액체 포장용 카톤 보드, 푸드 서비스용 카톤 보드), 포장 형태별(접이식 상자, 액체 포장, 슬리브 및 트레이 등), 최종 사용자 산업별(식품, 음료 등), 지역별(독일, 영국 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 카톤 보드 시장 동향 및 분석

PPWR 및 SUPD를 기반으로 한 플라스틱에서 섬유로의 대체

규정(EU) 2025/40은 2025년 2월 11일에 발효되며, 2026년 8월 12일부터 EU 회원국 27개국 전역에 적용됨에 따라, 유럽 카톤 보드 시장에는 지역 전체에 걸쳐 통일된 포장 관련 규정이 확립될 것입니다. 이 규정은 재활용에 중점을 둔 설계 기준, 재생 소재 함유율 의무, 그리고 확대 생산자 책임(EPR) 수수료 조정을 브랜드 소유자가 쉽게 미룰 수 없는 포장재 선택과 직접 연계함으로써, 기존의 지침 모델을 뛰어넘는 것입니다. 실무적으로는 이로 인해 복잡한 플라스틱 포장재의 재설계에 대한 압박이 커지는 반면, 많은 카톤 보드 포장재는 이미 이 새로운 체계 하에서 재활용 가능성 요건을 충족하고 있습니다. Mayr-Melnhof Karton AG는 이미 섬유 기반 소재를 포장 변경 프로그램을 추진하는 고객을 위한 전환 수단으로 자리매김하고 있으며, 이는 유럽 카톤 보드 시장에서 규제가 판매 과정의 일부로 자리 잡고 있음을 보여줍니다. Pro Carton이 2026년에 실시한 소비자 조사에 따르면, 유럽 응답자의 53%가 재활용이 불가능한 포장을 브랜드 변경의 이유로 꼽았으며, 이로 인해 소매업체의 사양과 브랜드 소유자의 일정이 같은 방향으로 추진되고 있습니다.

식품 소매 업계에서 재활용이 가능한 '진열대 정리' 패키지

독일, 프랑스, 영국의 식품 소매 업계에서 진행 중인 포장 프로그램에서는 매장 진열용 패키지의 형태가 재활용이 가능한 단일 소재의 카톤 보드 솔루션으로 전환되고 있으며, 점점 더 많은 카테고리에서 지속가능성이 단순한 브랜드 선호 사항에서 상품 입점의 상업적 조건으로 변화하고 있습니다. 이 점은 중요합니다. EPR(확대 생산자 책임) 수수료 조정으로 인해 재활용 가능한 포장이 점점 더 우대받고 있기 때문에 카톤 보드로의 전환에 따른 경제적 이점이 상품 진열상의 이점과 함께 고려되게 되었고, 이에 따라 사내에서 의사결정의 정당성을 입증하기가 쉬워졌기 때문입니다. 이러한 추세는 접이식 카톤 보드 수요를 촉진하고 있습니다. 왜냐하면 진열용 패키지의 경우, 인쇄성이 좋고 가공 효율이 높으며, 평량(g/㎡)이 줄어들어도 재활용이 용이한 형식이 선호되기 때문입니다. 네덜란드에서 열린 스마핏 웨스트록의 '2026 혁신 행사' 행사에는 450개 이상의 고객사가 모여, 디지털 개발을 통해 진열용 패키지의 맞춤 제작 주기가 어떻게 단축되고 있는지 입증하는 3종의 AI 기반 패키지 디자인 도구가 소개되었습니다. 이와 같은 논리는 현재 전자상거래 분야의 2차 포장 분야로도 확대되고 있습니다. 각 브랜드는 재설계를 최소화하고, 지속가능성에 대한 메시지를 보다 명확하게 전달할 수 있으며, 매장 진열부터 라스트 마일 배송까지 일관되게 사용할 수 있는 단일 카톤 보드 포맷을 원하고 있습니다.

에너지 및 펄프 비용의 변동, 특히 재생 등급의 경우

2026년에도 에너지 및 섬유 비용은 제조업체에게 여전히 가장 시급한 경영 과제로 남아 있었으며, 유럽의 카톤 보드 시장에서는 통합된 섬유 및 에너지 시스템에 의한 보호가 미흡한 등급에서 이러한 압박을 가장 크게 느꼈습니다. 비렐루드사는 2025년 4분기 실적 발표에서 유럽의 카톤 보드 원지 및 화이트탑 크라프트 라이너 공급 과잉으로 인해, 수요가 부진했고, 2026년 1분기까지 가격 압박이 지속됨에 따라 제지 업체들이 가격 책정을 통해 급등한 원자재 비용을 회수할 수 있는 능력이 제한되었다고 밝혔습니다. 공급 과잉과 공공요금의 변동이라는 이 두 가지 요인이 겹치면, 시장 상황이 불안정해졌을 때 이익 마진이 좁은 재생 카톤 보드 제조업체에게는 특히 힘든 상황이 됩니다. 또한 현물 가격의 추이를 예측하기 어려워지면, 구매자는 계약의 안정성과 공급의 일관성을 더욱 중시하게 되며, 가공업체의 구매 행동에도 변화가 생깁니다. 설비 가동률이 더욱 뚜렷하게 개선될 때까지는 유럽 카톤 보드 시장의 이익률 회복세가 등급이나 제조업체에 따라 편차를 보일 것으로 전망됩니다.

부문별 분석

2025년, 접이식 카톤 보드용 원지는 유럽 카톤 보드 시장 점유율의 33.91%를 차지했으며, 단일하고 폭넓은 가공 기반을 통해 식품, 의약품, 화장품 용도에 대응할 수 있다는 점에서 가장 큰 제품 등급이 되었습니다. 이러한 선도적인 위상은 오프셋 인쇄, 디지털 인쇄, 플렉소 인쇄와의 호환성을 반영하고 있으며, 이 등급의 제품은 일상적인 식료품 포장부터 고부가가치 소매용 디스플레이 형태에 이르기까지 최소한의 마찰로 전환할 수 있습니다. 이러한 규모는 확립된 가공업체의 인프라와, 해당 지역의 대부분에서 이미 접이식 카톤 보드를 우선적으로 사용하는 '진열대 정리'의 소매 사양에 의해 뒷받침되고 있습니다. 핀란드의 스트라 엔소(Stora Enso)사가 10억 유로(10억 8,000만 달러)를 투자해 건설한 오울루 생산 라인을 통해 연간 75만 톤의 생산 능력이 추가되었으며, 메차 보드사가 2억 1,000만 유로(2억 2,700만 달러)를 투자해 실시한 후스무 공장 확장으로 연간 20만 톤의 생산 능력이 추가되었습니다. 이로 인해, 새로운 공급이 시장에 흡수되고 있는 현 상황에서 단기적인 가격 회복에 큰 부담이 되고 있습니다. 솔리드 표백지는 외식 산업, 의약품 포장, 고급 화장품 분야에서 계속해서 프리미엄 시장을 차지하고 있는 반면, 솔리드 미표백지는 산업용 및 내구성이 요구되는 용도에서 여전히 틈새 시장으로 머물러 있습니다. 또한, 외식 산업용 카톤 보드는 2026년 8월 규제 준수 기한에 앞서 PFAS가 포함되지 않은 성분으로의 변경이 진행되고 있습니다.

액체 포장용 카톤 보드는 2026-2031년 연평균 성장률(CAGR) 5.17%로 확대될 것으로 예상되며, 유럽의 카톤 보드 시장에서 가장 빠르게 성장하는 제품 등급이 될 전망입니다. 테트라팩과 스텔릴가르다 알리멘티는 2026년 4월, 종이 기반 차단층을 갖춘 1리터 무균 카톤을 출시했으며, 이는 알루미늄이 포함되지 않은 카톤 기술로서는 최초의 산업 규모 실증 사례가 되었습니다. 또한, 테트라팩은 2030년까지 매년 1억 유로(1억 900만 달러)를 지속 가능한 포장 개발에 투자할 계획의 일환으로, 스웨덴 룬드에 종이 기반 배리어 소재의 시범 공장에 6,000만 유로(6,500만 달러)를 투자하기로 결정했습니다. 이는 액체용 카톤 기술이 얼마나 빠르게 발전하고 있는지를 여실히 보여주고 있습니다. 또한, 수요가 종이 사용량이 많은 음료 포맷으로 전환되는 가운데, 각 제조업체들은 효율성, 품질 관리, 제품의 유연성을 높이기 위해 액체용 카톤 보드의 핵심 자산을 업그레이드하고 있습니다. 화이트 라이닝 처리가 된 칩보드는 여전히 가격에 민감한 2차 포장용으로 사용되고 있지만, 유럽의 전체 카톤 보드 시장에서 에너지 비용과 비용 가시성이 불안정해짐에 따라 그 상대적 위상은 약화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the europe cartonboard market size is projected to be USD 13.17 billion in 2025, USD 13.63 billion in 2026, and reach USD 16.42 billion by 2031, growing at a CAGR of 3.79% from 2026 to 2031.

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), End-User Industry (Food, Beverage, and More), and Geography (Germany, United Kingdom, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Cartonboard Market Trends and Insights

Plastic-To-Fiber Substitution Under PPWR And SUPD

Regulation (EU) 2025/40 entered into force on February 11, 2025, and will apply across all 27 EU member states from August 12, 2026, giving the Europe cartonboard market one common packaging rulebook across the region. The regulation goes beyond the earlier directive model by tying design-for-recycling criteria, recycled-content obligations, and EPR fee modulation directly to packaging choices that brand owners cannot easily delay. In practical terms, this places greater pressure to redesign complex plastic formats, while many carton formats already meet recyclability expectations under the new framework. Mayr-Melnhof Karton AG has already positioned fiber-based materials as transition tools for customers working through packaging change programs, showing how regulation is becoming part of the sales process in the Europe cartonboard market. Pro Carton found in its 2026 consumer survey that 53% of European respondents cited non-recyclable packaging as a reason for brand switching, which is pushing retailer specifications and brand-owner timelines in the same direction.

Recyclable Shelf-Ready Packs In Food Retail

Food retail packaging programs in Germany, France, and the United Kingdom are moving shelf-ready formats toward recyclable mono-material carton solutions, turning sustainability from a brand preference into a commercial listing condition in more categories. This matters because EPR fee modulation increasingly rewards recyclable packaging, so the financial case for carton conversion now sits alongside the merchandising case, making decisions easier to justify internally. The effect supports folding boxboard demand because shelf-ready packs favor formats that print well, convert efficiently, and remain easy to recycle even when basis weights are reduced. Smurfit Westrock's 2026 Innovation Event in the Netherlands brought together more than 450 customers and introduced 3 AI-based packaging design tools that demonstrate how digital development is shortening customization cycles for shelf-ready packaging. The same logic now extends to e-commerce secondary packaging, where brands want one cartonboard format that can move from shelf display to last-mile shipment with minimal redesign and a clearer sustainability claim.

Energy And Pulp Cost Volatility, Especially In Recycled Grades

Energy and fiber costs remained the most immediate operating challenge for producers in 2026, and the European cartonboard market felt that pressure most sharply in grades with less protection from integrated fiber and energy systems. Billerud stated in its Q4 2025 results that overcapacity in cartonboard and white top kraftliner in Region Europe kept demand subdued and price pressure visible into Q1 2026, limiting mills' ability to recover higher input costs through pricing. That combination of loose supply and volatile utilities is especially difficult for recycled-board producers because they have less margin room when market conditions turn unstable. It also changes converter purchasing behavior, with buyers placing more value on contract stability and supply consistency when spot pricing becomes harder to read. Until capacity utilization improves more clearly, margin recovery in the European cartonboard market is likely to remain uneven across grades and producer types.

Other drivers and restraints analyzed in the detailed report include:

- Pharmaceutical Serialization And Tamper-Evident Cartons

- Premium Beauty And Personal Care Carton Upgrading

- Reuse And Packaging-Minimization Rules Capping Unit Growth

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard held 33.91% of the European cartonboard market share in 2025, making it the largest product grade because it can serve food, pharmaceutical, and cosmetics applications through a single broad converting base. Its leading position also reflects its compatibility with offset, digital, and flexographic printing, enabling the grade to move from everyday grocery packaging into higher-value retail presentation formats with minimal friction. That scale is supported by established converter infrastructure and by shelf-ready retail specifications that already favor folding boxboard across much of the region. Stora Enso's EUR 1 billion (USD 1.08 billion) Oulu line in Finland added 750,000 tonnes of annual capacity, and Metsa Board's EUR 210 million (USD 227 million) Husum expansion added 200,000 tonnes annually, which has weighed on near-term price recovery while new supply is still being absorbed. Solid bleached board continues to occupy the premium tier in food service, pharmaceutical packaging, and luxury beauty work, while solid unbleached board remains more niche in industrial and heavy-duty uses, and food service board is moving through PFAS-free reformulation ahead of the August 2026 compliance date.

Liquid packaging board is projected to expand at a 5.17% CAGR from 2026 to 2031, making it the fastest-growing product grade in the European cartonboard market. Tetra Pak and Sterilgarda Alimenti launched a 1-liter aseptic carton with a paper-based barrier in April 2026, providing the first commercial industrial-scale proof point for aluminum-free carton technology. Tetra Pak also committed EUR 60 million (USD 65 million) to a paper-based barrier pilot plant in Lund, Sweden, as part of its plan to invest EUR 100 million (USD 109 million) annually through 2030 in sustainable packaging development, underscoring how quickly the liquid carton technology frontier is advancing. Producers are also upgrading core liquid board assets to improve efficiency, quality control, and product flexibility as demand shifts toward more paper-intensive beverage formats. White-lined chipboard still serves price-sensitive secondary packaging, but its relative position is weaker when energy costs and cost visibility become less stable across the European cartonboard market.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

List of Companies Covered in this Report:

- Metsa Board Corporation

- Stora Enso Oyj

- Mayr-Melnhof Karton AG

- Billerud Aktiebolag

- Sappi Limited

- RDM Group S.p.A.

- WEIG-Karton GmbH & Co. KG

- Iggesund Paperboard AB

- Kotkamills Oy

- Pankaboard Oy

- Graphic Packaging International, LLC

- Smurfit Westrock plc

- Mondi plc

- Van Genechten Packaging NV

- Edelmann Group GmbH

- Tetra Pak International S.A.

- SIG Group AG

- Elopak ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Plastic-to-Fiber Substitution Under PPWR and SUPD

- 4.2.2 Recyclable Shelf-Ready Packs in Food Retail

- 4.2.3 Pharmaceutical Serialization and Tamper-Evident Cartons

- 4.2.4 Premium Beauty and Personal Care Carton Upgrading

- 4.2.5 QR-Enabled Compliance and Digital Labeling on Pack

- 4.2.6 PFAS-Free Barrier Migration in Food Service Board

- 4.3 Market Restraints

- 4.3.1 Energy and Pulp Cost Volatility, Especially in Recycled Grades

- 4.3.2 Reuse and Packaging-Minimization Rules Capping Unit Growth

- 4.3.3 Compliance Data Burden for Small and Mid-Sized Converters

- 4.3.4 Lightweighting Reducing Tonnes Faster Than Unit Demand

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Trade Flow and Capacity Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Metsa Board Corporation

- 6.4.2 Stora Enso Oyj

- 6.4.3 Mayr-Melnhof Karton AG

- 6.4.4 Billerud Aktiebolag

- 6.4.5 Sappi Limited

- 6.4.6 RDM Group S.p.A.

- 6.4.7 WEIG-Karton GmbH & Co. KG

- 6.4.8 Iggesund Paperboard AB

- 6.4.9 Kotkamills Oy

- 6.4.10 Pankaboard Oy

- 6.4.11 Graphic Packaging International, LLC

- 6.4.12 Smurfit Westrock plc

- 6.4.13 Mondi plc

- 6.4.14 Van Genechten Packaging NV

- 6.4.15 Edelmann Group GmbH

- 6.4.16 Tetra Pak International S.A.

- 6.4.17 SIG Group AG

- 6.4.18 Elopak ASA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment